Using Machine Learning To Accelerate Trading Strategy Discovery

The Hunt For Alpha & The Q2 Incubator

Important: There is no guarantee that ATS strategies will have the same performance in the future. I use backtests and forward tests to compare historical strategy performance. Backtests are based on historical data, not real-time data so the results shared are hypothetical, not real. Forward tests are based on live data, however, they use a simulated account. Any success I have with live trading is untypical. Trading futures is extremely risky. You should only use risk capital to fund live futures accounts and if you do trade live, be prepared to lose your entire account. There are no guarantees that any performance you see here will continue in the future. I recommend using ATS strategies in simulated trading until you/we find the holy grail of trade strategy. This is strictly for learning purposes.

I know we’ve had an influx of new subscribers over the last month. So as a quick reminder, we’re on the hunt for the holy grail of automated trading strategy. If you have any questions, start with the FAQs and if you still have questions, feel free to reach out to me (Celan) directly at AutomatedTradingStrategies@protonmail.com.

The Nobel Prize in Chemistry was divided in 2024: one half was awarded to David Baker "for computational protein design"; the other half jointly to Demis Hassabis and John Jumper "for protein structure prediction".

Demis Hassabis is also Google Deepmind’s CEO, and he gave a fascinating lecture in acceptance of the award. The title of the lecture: "Accelerating scientific discovery with AI".

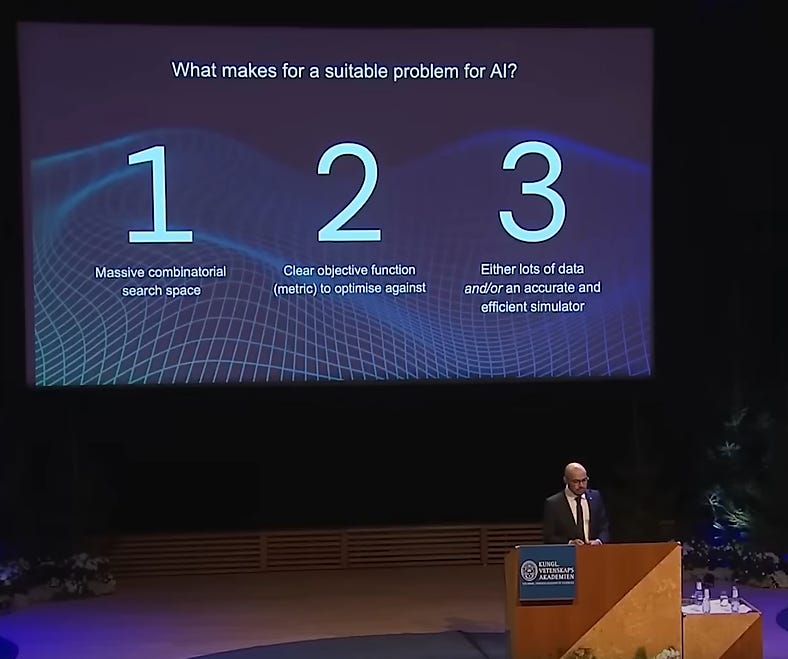

This is the slide that caught my eye.

This slide is showing three criteria that make a problem well-suited for AI:

Massive combinatorial search space

Clear objective function (metric) to optimize

Either lots of data and/or an accurate and efficient simulator

While hardly as noble as computational protein design or protein structure prediction, the requirements map directly onto automated/algorithmic trading: lots of possibilities to explore, a clear objective (returns), and abundant data.

Financial markets present a huge range of possible trades. AI systems can sift through countless permutations—across various instruments, time frames, and economic conditions. Likewise, traders typically have a very clear objective—maximize returns, minimize losses. This provides an explicit signal that an AI can optimize against. And we have so much data it’s hard to find a file format that can handle it all.

The simulator part is a work-in-process, however. I’m currently testing the use of machine learning models to develop strategies based on simulated market data and then verifying the answer with actual data, which triggers an adjustment to the simulation. The idea was inspired by Grok 3, which used simulated data to train on, and actual data to verify against.

So the good news is that our hunt is a natural application for AI methods. The challenge is in the application.

“But your weakness is not your technique.”

Morpheus, From ‘The Matrix’

Applying ML To The Strategy Creation, Selection & Improvement Process

At the beginning of 2024 I started my first Live Test. I hope to conduct another, but this year I wanted to devote more time to studying the application of ML to trading. I believe it has the ability to take our hunt to new heights.