How Much Do You Need To Start Trading An Automated Trading Strategy?

This has become the new ‘commonly asked question’, so we thought we’d address it directly. We talk a little about it here with regard to the difference between reinvestment and total investment when trading futures, but not head on. In this post we’re going to provide some ways to think about how much you need to get started trading automated strategies. When we say “get started” we are referring to the amount you need before you enable the strategy. You can withdraw funds from your account, but you never want to go below a certain level and the goal of this post is to help you determine that level.

First, we need to get a little housekeeping of the way:

There is no right answer to this question because not everyone has the same risk profile. Some will find our recommendation overly cautious, while others will find it to be risk friendly. You can use your own reaction to the recommendations in this post as a way to know which camp you’re in.

There is no guarantee that automated strategies will perform the same in the future. We use backtests to gauge performance, but there are no guarantees. This matters because we use backtest performance, specifically the max cumulative drawdown, as a way to determine how much you need to trade each strategy. In other words, the amount you need depends on the strategy’s performance — there is no standard amount.

We are looking for the holy grail of trade strategy for the NASDAQ futures contract (NQ). This is our current hunt. It is an ambitious hunt, we know, but it is where we’ve decided to start. Since drawdown is driven by volatility, and the NQ futures contract is one of the most volatile contracts on the market, the amount you will need to trade our strategies with an NQ futures contract will likely be more than it would be if trading other futures contracts. In other words, this is a high risk hunt, and we are risk adverse by nature, but we’re interested because the rewards match the hunt.

With that out of the way, let’s get to it.

How Much Do You Need

In general, we recommend a trading account that is at least equal to the cumulative max drawdown. The cumulative max drawdown is the lowest your account value has ever dropped from its high. So, if the account value starts off at $50K and grows to $51K the next day, and then $55K on day 3, and then $60K on day 4, before dropping back to $50K on day 5, the cumulative max drawdown is $10K, not $0. This is telling you that you need to have at least $10K in your account to withstand the drawdown. Why? Because day 5 could have been day 2.

Our backtests consist of 365 days or 253 trading days. So instead of knowing what the drawdown statistics are for only 5 days, we know what they are for 253 trading days. The max drawdown that we list on our performance chart provides the lowest drawdown the strategy has ever had over the course of those 253 days. For this reason, we like to use it as a lower limit on the value of the account.

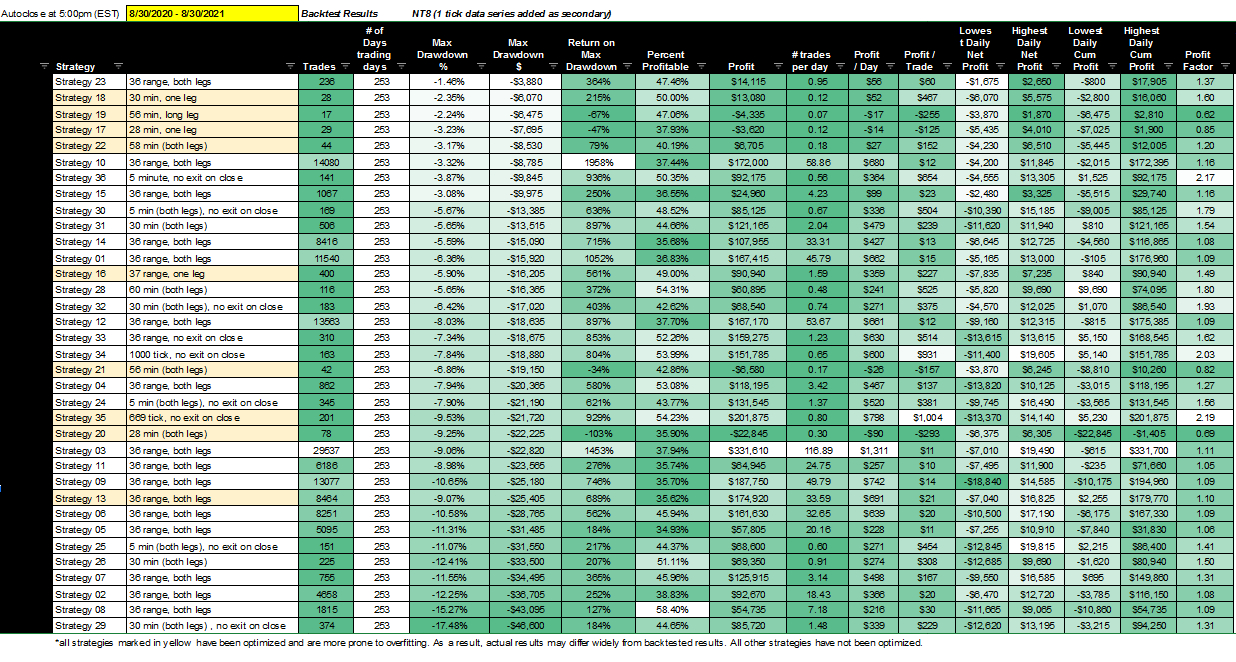

Here’s the performance chart sorted by max cumulative drawdown. Please click on the chart to enlarge.

Strategy 23 has the lowest cumulative max drawdown at -$3,880. It also has one of the lowest net profit metrics at $14K. We’re talking $56/day or $60/trade. Not bad, but not great either.

We’re going to advise skipping over Strategies 18, 19, 17 and 22. These are optimized strategies and we’ve found that they tend to have inconsistent results.

Before moving on to our next strategy, however, let’s review two other metrics that can help to understand how much you need to trade the strategy: max drawdown % and return on max drawdown.

The cumulative max drawdown % may not be what you think. Intuitively, you may think it refers to the drawdown % based on the original account value, but this is false. It refers to the high reached before the drawdown. So, if a strategy has a max drawdown of 5%, it is not referring to 5% of the account value, but rather 5% of the high from which the drawdown started. This can be confusing to some, but it’s a way of showing what the drawdown is regardless of account size.

Return on cumulative max drawdown is calculated by dividing net profit by the cumulative max drawdown. In this way, max drawdown is used as a proxy for max capital investment. Another way to think about max capital investment is the amount you need to trade the strategy. In general, the higher the return on max drawdown, the better the strategy is in terms of risk/reward.

With the help of these two additional metrics, along with the strategy’s profit factor, we can triangulate into a way to calculate how much you need to start a particular strategy.

The next strategy on the list, coming in at #2 (after excluding optimized strategies) is Strategy 10. Strategy 10 has a max drawdown of -$8,785 for the year, but it made $172K in net profit. This is why the strategy has a return on max drawdown of 1958%, it is the highest return on max drawdown of all our strategies. That said, this is a strategy that is best traded on a flat rate commission plan because it makes ~58 trades per day. It also has a relatively low profit factor of 1.16, which leaves little room for error. Still, because the max drawdown is low, you could trade this strategy with a $9K account. Of course, you want to give yourself a buffer (to account for slippage, margin, low profit factor, etc) so we would recommend a $15K account. What does this mean? It means you can take as much as you want out of the account as long as you leave $15K to trade.

Let’s analyze one more strategy for good measure. Coming in at #3 is Strategy 36. Strategy 36 is one our best strategies because of its low cumulative max and high return on cumulative max drawdown. It has a return on max drawdown of 936% — only Strategies 1, 3 and 10 have a higher return on max drawdown, but unlike these strategies the profit per trade is $654 rather than $15, $11 and $12, respectively. This is primarily due to the strategy’s maximum favorable excursion (MFA), which is almost two times higher than its maximum adverse excursion (MAE) -- to learn more about MFA, MAE and ETD statistics, click here. In other words, it has a very effective entry command. It also has one our highest profit factors at 2.17. If you wanted to trade this strategy, you would need at least a $10K account. Again, you want to give yourself a buffer so we would recommend a $15K account. This is telling you how much you want to have in the account while running it. You can take out as much as you want, but make sure you leave at least $15K in the account to withstand the drawdown swings.

Something else we want to point out about Strategy 36 is that while the max drawdown is -$9,854, the account value never drops below $1,525. This is due to when the strategy was started more than anything else. As discussed in the example given above regarding drawdown, if Day 5 is switched with Day 2, you have the same drawdown, but you go from having an account that never drops below $0, to an account that dropped to -$10,000. All this to say, like any race, when and how you start is important. Don’t just start on Sunday night when the market opens, wait until the day or the day before (and if possible the hour) that has been shown to result in the highest income.

‘What If I Don’t Have $15K’

Some of you may be saying, ‘this is great, but I don’t have $15K’. First, please keep in mind that trading is very risky in general. If you need the money in your account to live (food, rent, bills, etc), do not use it to trade. Every trader has used money they didn’t have to trade. I talk about how I lost $10K when I first started trading in the post: Trading Is A Dark And Scary Forest.

When I first started trading, I traded with money I could not afford to lose and was financially devastated when I lost it. So, the hardest lesson to learn for any decent trader is to never trade with money you need.

The good news is that there are other options now. Today you have the option of trading e-mini contracts. The MNQ contract is the e-mini version of the NQ contract. With an e-mini MNQ contract the value of each tick is 1/10th the size of a regular NQ contract. So instead of $5 per tick, it’s $.50 per tick. This will greatly lower your net profit, but it will also lower your cumulative max drawdown and therefore the amount you can trade. The same rules apply — you still can’t trade with funds you need, but it lowers the bar a bit to make that threshold more attainable. Again, you never want to trade with money that would be a hardship if you lost it.

The following is a performance chart of the MNQ contract over the same backtest period.

Once again, Strategy 23 stands out with the lowest drawdown of -$602 — that’s for the entire year. That means you would want to have at least a $700 account to trade Strategy 23 using 1 MNQ contract. Of course, you want to give yourself a buffer so we would recommend at least a $2K account. That may sound great from a drawdown perspective, but it also only makes $1,060 for the year. This is one reason why the return on max drawdown for Strategy 23 is only 176%.

If we were going to trade the MNQ, we would probably trade Strategy 33. It has a profit per trade of $71, which is higher than some of our strategies when traded on an NQ futures contract. It also has a cumulative max drawdown of -$1,793 and a return cumulative max drawdown of 856%. You would need at least an $1,800 account to trade this strategy, but you want to give yourself a buffer so we would recommend a $4-$5K account.

One last thing — you will notice a slight deterioration in profit factor for MNQ statistics compared to NQ stats. It is difficult to say why this is exactly, but in general, the market is skewed toward size. That is, the more there is of something (quantity/volume), the better the trading pattern will be. This also plays out with time. That is, the more time your chart covers, the better, or the more consistent, the pattern is. While each e-mini contract should trade exactly like its big sister, each market has its own mind. We’ve tried to take advantage of the price divergence between the two markets (MNQ and NQ), but the profits were very small. We believe there are already algorithmic systems in place that arbitrage this divergence, making it difficult for retail traders to gain an edge.