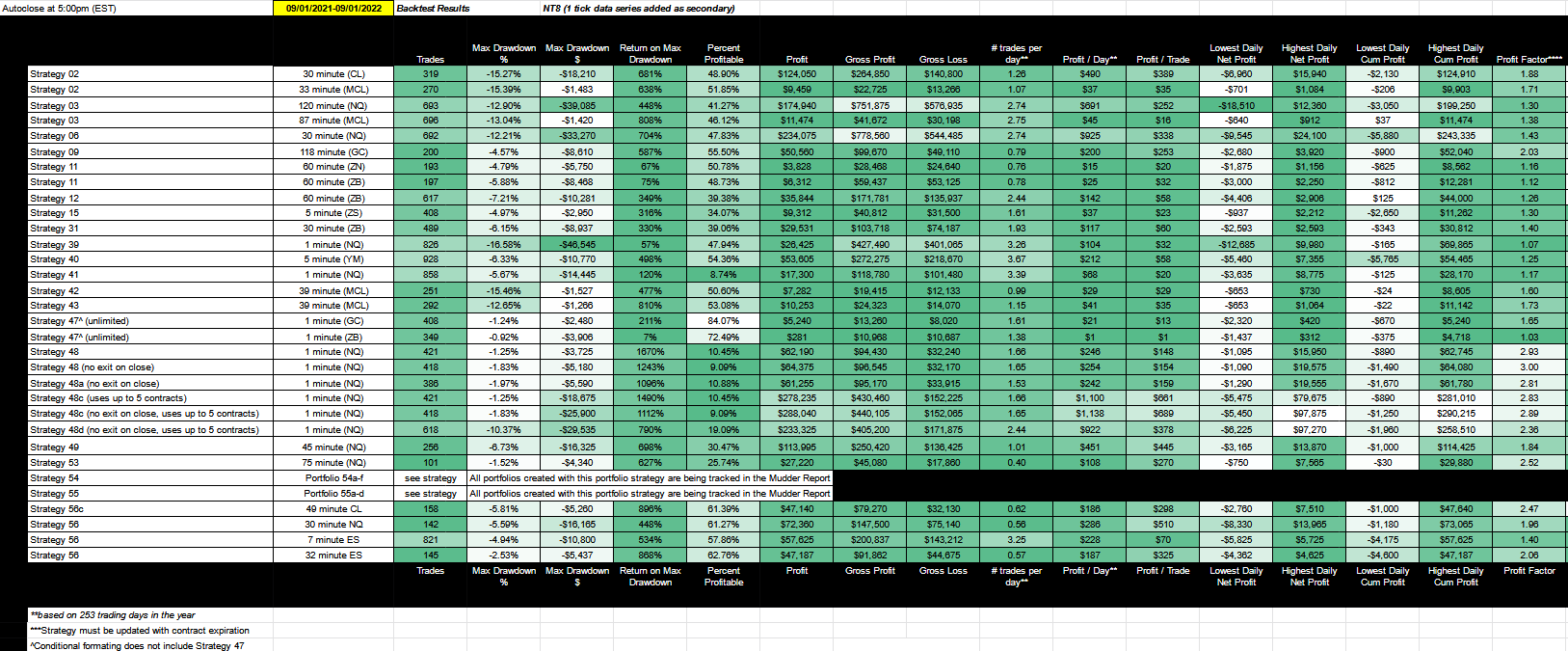

Automated Trading Strategy #56

Strategy 56 is profitable 62% of the time. It made $72K based on a 1 year backtest period using 1 NQ contract. It has a profit factor of 1.96 and a Sortino ratio of 1.88.

There is no guarantee that these strategies will have the same performance in the future. Some may perform worse and some may perform better. We use backtests to compare historical strategy performance. Backtests are based on historical data, not live data. There are no guarantees that this performance will continue in the future. Trading futures is extremely risky. If you trade futures live, be prepared to lose your entire account. We recommend using our strategies in simulated trading until you/we find the holy grail of trade strategy.

Click on the table to enlarge.

As a quick reminder, our goal is to find the holy grail of automated trade strategy as defined below:

Profit factor greater than 3

Annual drawdown less than 3%

Annual return on max drawdown greater than 500%

Maximum daily net loss of -$1,000

Avg Daily profit greater than $1,000

Less than 5,000 trades annually

More than 253 trades annually

We haven’t found the holy grail yet, but we get closer with every strategy. For a link to all strategies and the most recent chart, click here.

Is the holy grail of automated trade strategy a myth?

What would you do to take a picture of a unicorn or Bigfoot? What would you do to lay eyes on a real alien? If Bigfoot and aliens aren’t your fancy, how about the the ghost of a loved one or a fairy from the Tuatha dé Danann? I wouldn’t mind taking a picture with the demigod Thoth, but I digress.

These are all myths. Some are more real and powerful to us than others. I know that some of you don’t believe that the holy grail of automated trading strategy exists. You say this hunt is a waste of time, but I think you’re wrong.

The truth is, what we’re hunting is more tangible than any of the myths above. We know much more than our critics would like to admit.

What do we know?

Let’s take stock of what we already know. We know where the creature called “price” was a moment ago. That moment can be as small as one millisecond (one tick). And, if we’re honest, what we’re looking for isn’t really where the creature is now or even an instant from now. What we want is something that will tell us where the creature will be some time in the future. This is what makes the creature so elusive.

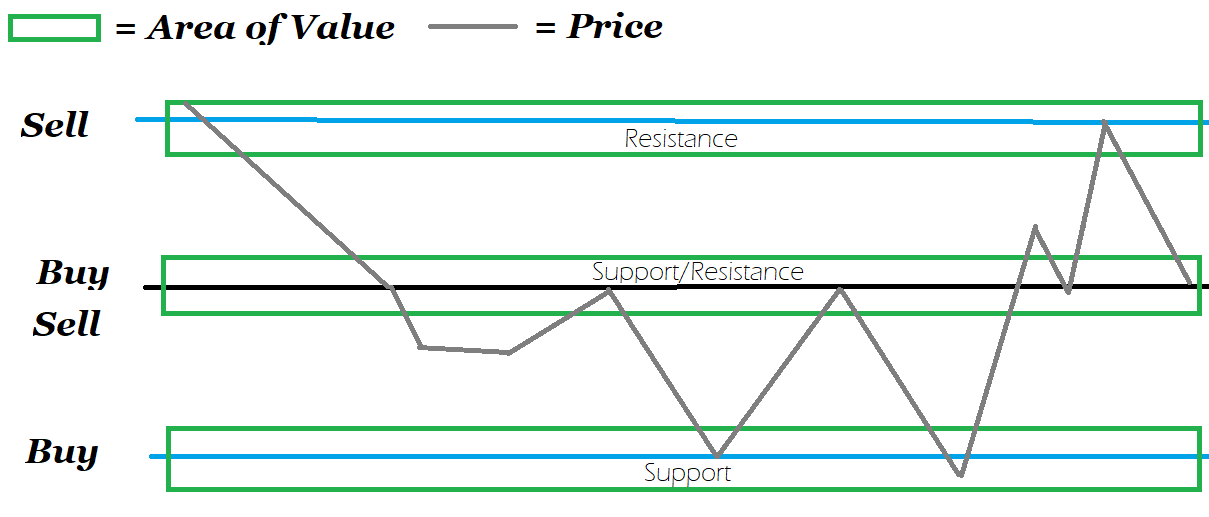

The good news is that unlike traders from 100 years ago, we have an incredible amount of data at our disposal. We know the size (volume) of the creature; we know the path the creature generally takes (moving average), and we can even create a kind of radius around this path (standard deviation from the moving average or mean). We also know that there are certain areas in the forest that are harder to pass (rivers, mountains). The creature will only go beyond these areas when pushed. In trading these areas are referred to as points of resistance and support and they represent “high value areas”. These are places where traders like to set orders and wait for the price to come to them.

The image below is my attempt at illustrating these relationships.

These are the relationships that Strategy 56 takes advantage of. It identifies and places trades around high value areas.

The hardest thing about this strategy is defining which moving average to use. You have to find the one that institutional traders use as well for it to work. It should look like the blue line in the chart below:

As you can see, this line acts as both a point of support and resistance.

Then you’ll need to figure out a way to define the areas of value around this line. That’s what we did with Strategy 56. Then we ran the strategy across a range of futures contracts and optimized based on data series (1-60 minute). Across the board, this strategy shows an edge. The percentage of profitable trades are all higher than 55%, average profit factor is 1.61, and the average Sortino Ratio is 1.69 on 2382 trades for the total portfolio.

As a quick review, the Sortino ratio is like the Sharpe ratio — both are considered to be measures of risk adjusted return. You can read about how NinjaTrader defines them here. Ultimately, both are a measure of return based on risk and risk is defined as the standard deviation of your return profile. Higher standard deviation equates to higher risk.

Why do I prefer the Sortino ratio? There’s no getting around the inherent risk involved in trading highly volatile markets like the one we’re in now, but you can improve your performance by looking for strategies that reward you for taking on that risk. Unlike Sharpe, the Sortino ratio is more concerned with negative volatility or downside risk than total volatility. In the same way that all slippage isn’t bad, all volatility isn’t bad either. The Sortino ratio only factors in the downside standard deviation in its calculation and is therefore better to evaluate high-volatility strategies, whereas the Sharpe ratio is good for evaluating low-volatility portfolios.

A negative Sortino ratio is bad. It means that the risk-free rate is higher than the portfolio's return — yikes. A ratio between 0 and 1 is considered sub-optimal; higher than 2 is considered very good; and, higher than 3.0 is considered excellent.

Highlights within the portfolio:

1 CL futures contract: one year backtest performance (158 trades) - profit factor of 2.47 on $47K (annual), with a 4.54 Sortino ratio, and 61% profitable trades

1 NQ futures contract: one year backtest performance (142 trades) - profit factor of 1.96 on $72K (annual), a 1.88 Sortino ratio, and 62% profitable trades

Now, let’s talk about how to recreate Strategy 56.

Strategy 56 Description, Command Structure & Download (C#)

Strategy 56 uses two of my favorite indicators: