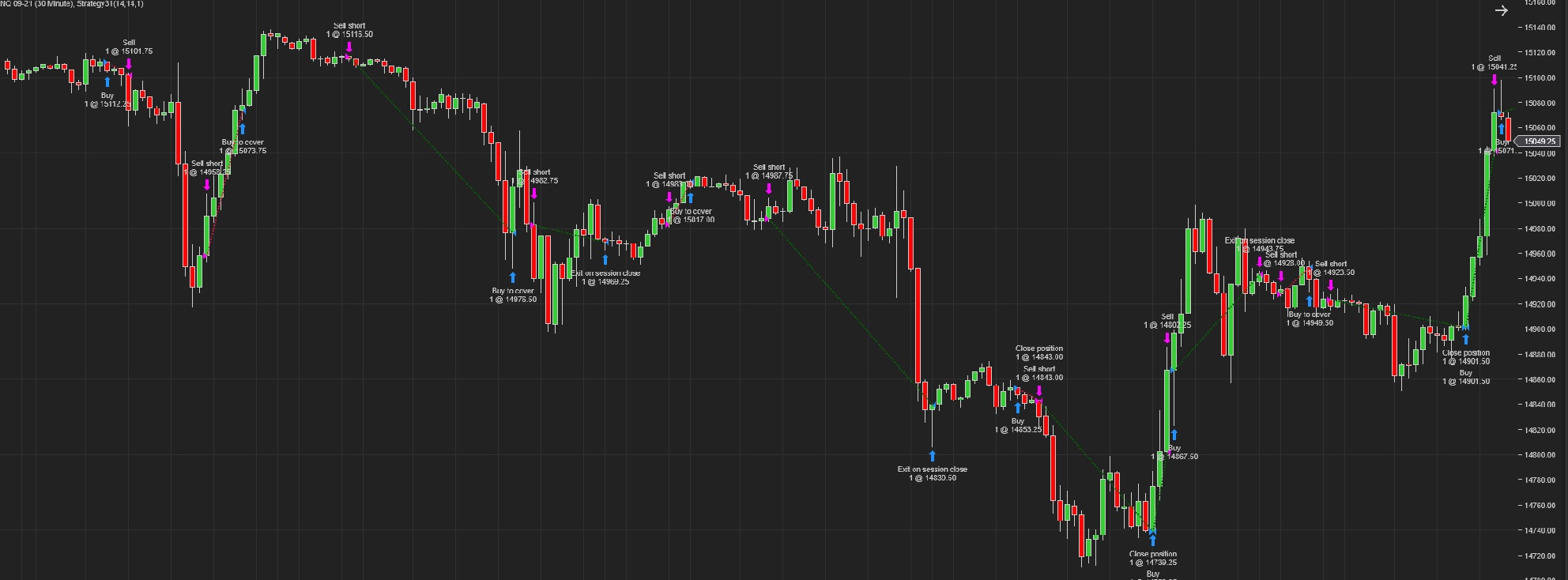

Automated Trading Strategy #31

Strategy 31 made $120K in the last 12 months, makes $233 per trade and has a Profit Factor of 1.52.

There is no guarantee that these strategies will have the same performance in the future. Some may perform worse and some may perform better. We use backtests to compare historical strategy performance, but there are no guarantees that this performance will continue in the future. Trading futures is extremely risky. If you trade futures live, be prepared to lose your entire account. We recommend using our strategies in simulated trading until you/we find the holy grail of trade strategy.

For a link to all strategies and the most recent chart, click here.

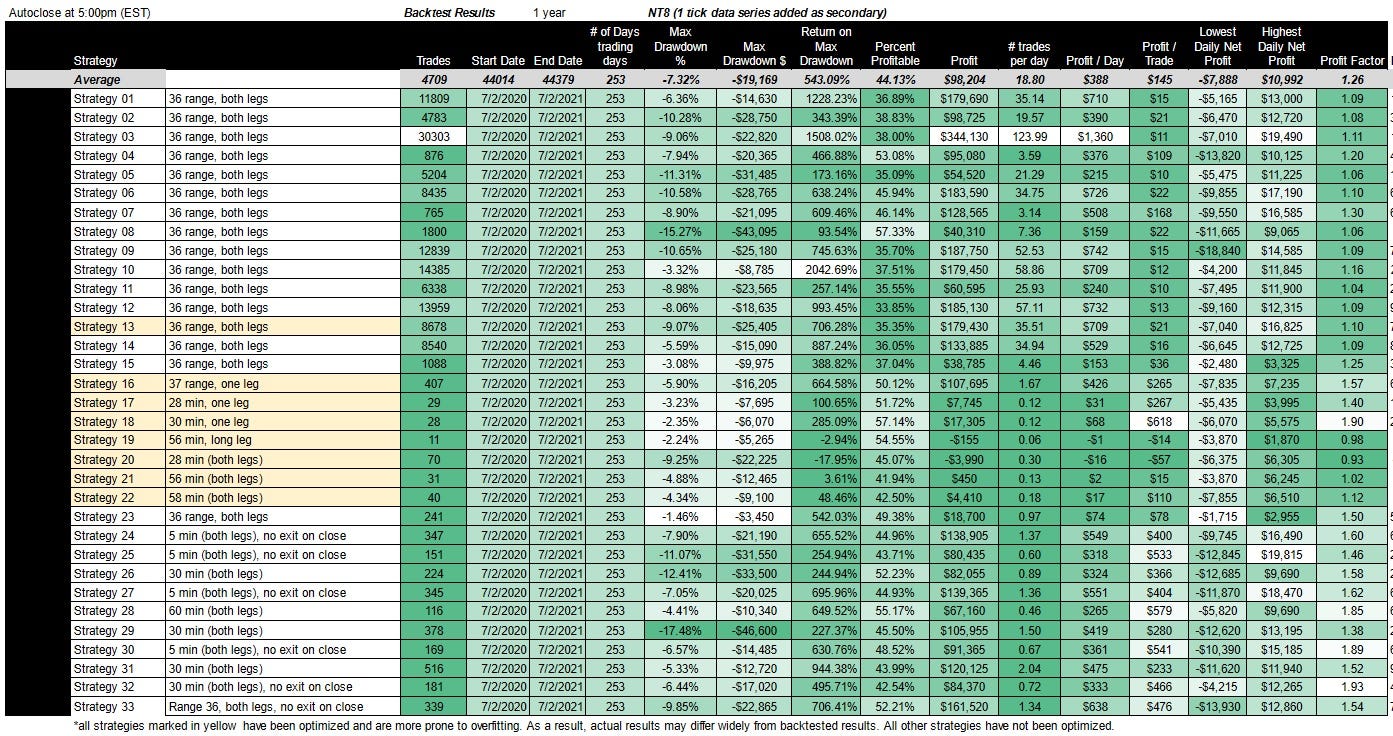

Click on the table to enlarge.

*See below for Column Definitions

Strategy #31 Description:

Subscribers: Click here for the Subscriber-only version of this strategy description, which includes a full description of the strategy as well as the NT8 download.

This is what the strategy looks like in chart form. Over a 1 year period, it makes on average 2 trades per day and has an average net profit of $475 per day or $233 per trade:

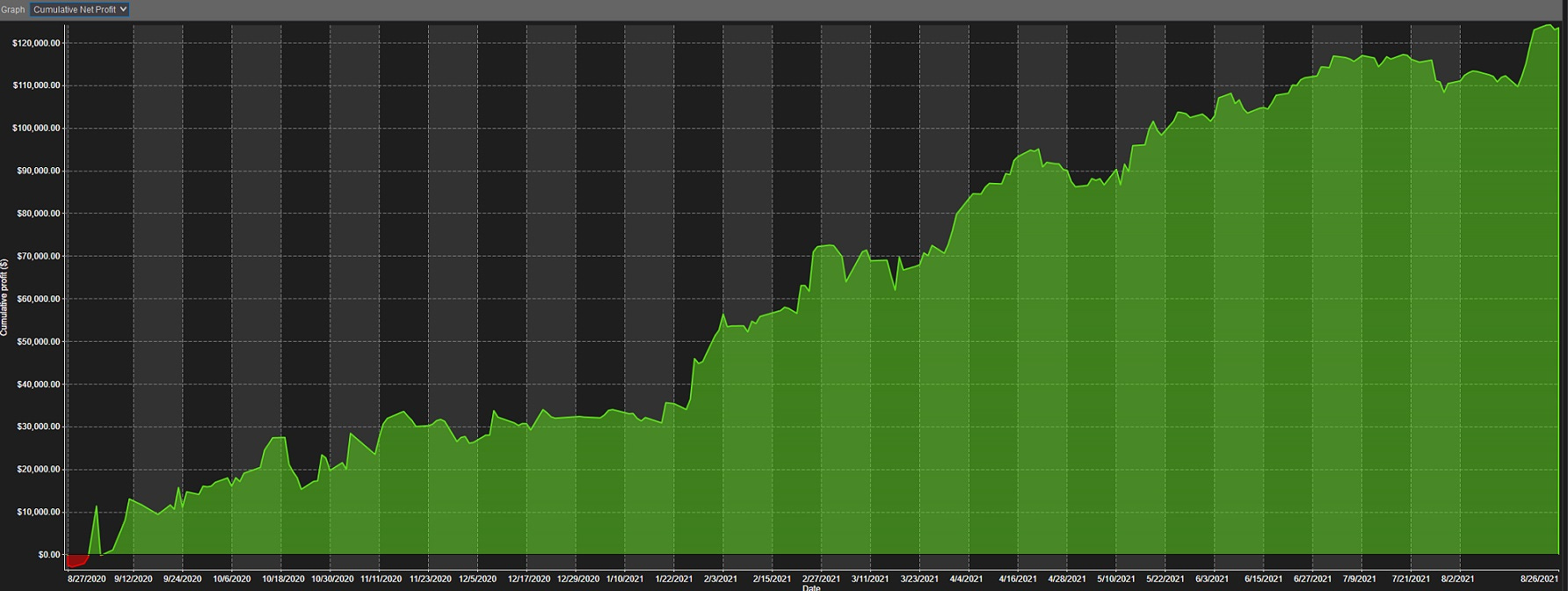

This is the cumulative profit of Strategy 31 over a 1 year period. It has the profit profile we like to see — a slow and gradual growth pattern with few dips. It starts off with a slight dip below zero, reaching a cumulative low of only $85, but then continues to grow over zero from that point on. Max drawdown is therefore relatively low at 5.33% or $12,720.

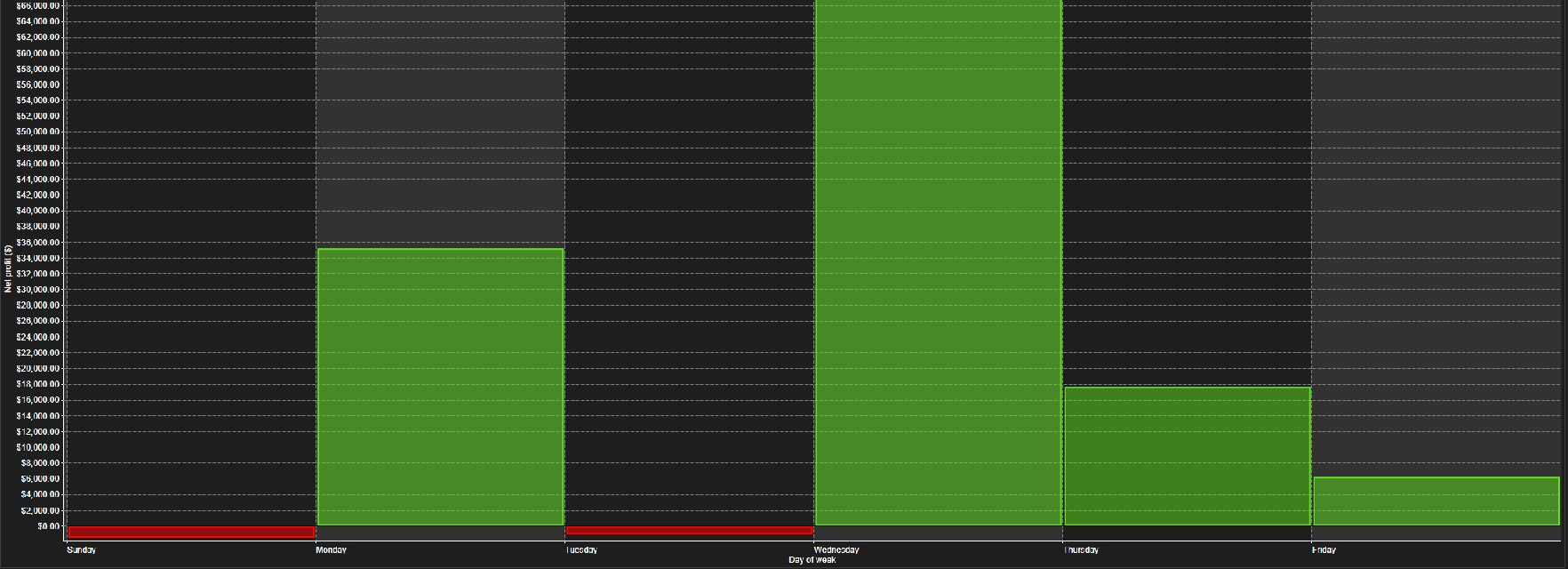

This is how the strategy breaks down on a day-of-week basis. Wednesday is clearly the most profitable day followed by Monday.

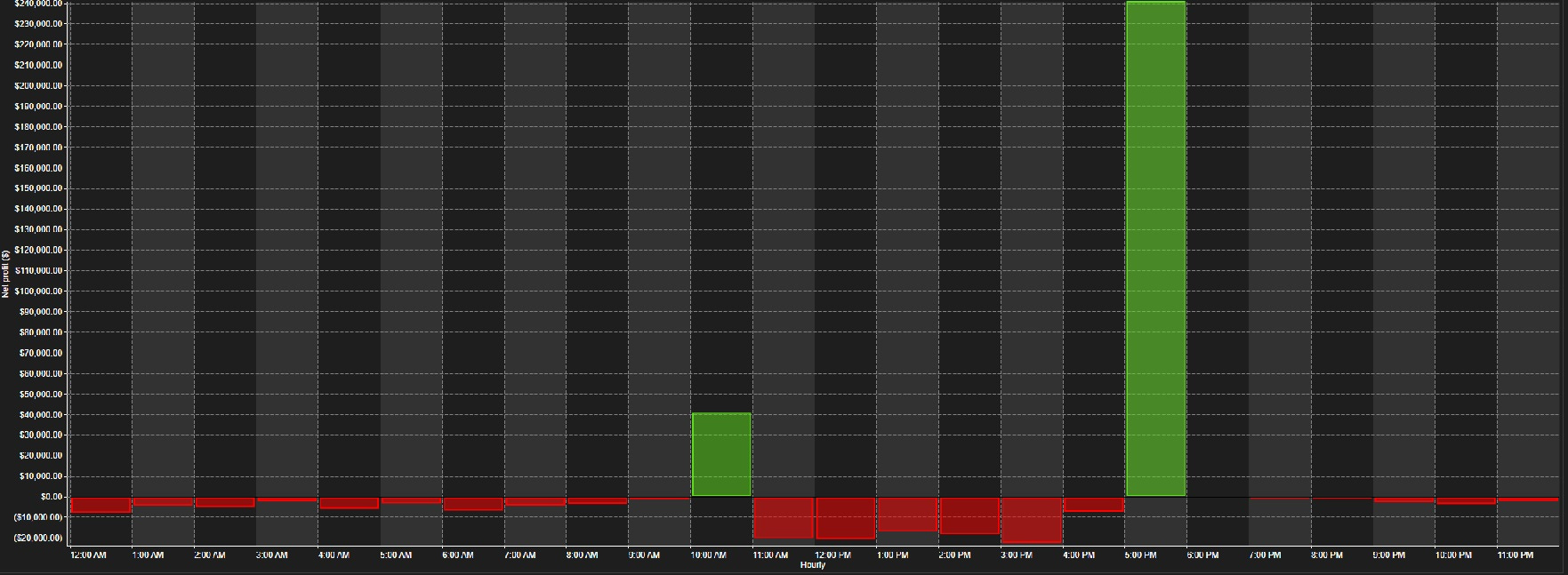

This is a chart of the strategy by hour of day. Keep in mind, this strategy closes at the end of each day.

We like this strategy because of its high profitability and low drawdown. It boasts high net profitability along with a high profit factor and makes over 500 trades per year. It also has one of the highest returns on max drawdown at 944%.

The hunt continues, but this is one of our favorite strategies. We will definitely continue to build on the concepts used within its logic.

For links to all strategies click here.

Download Strategy #31 for NinjaTrader 8:

Subscribers: Click here for the Subscriber-only version of this strategy description, which includes a full description of the strategy as well as the NT8 download.

*Column Definitions:

Strategy - The name of the strategy.

Trades - The number of trades used in the backtest to analyze performance. Our goal is ~1,000 trades for comparison.

Start date- The beginning date of the backtest.

End date - The ending date of the backtest.

# of days - The number of days in the strategy.

Drawdown - This refers to the maximum drawdown statistic, which provides you with information regarding the biggest decrease (drawdown) in account size experienced by the strategy. Drawdown is often used as an indicator of risk.

Drawdown = single largest Drawdown

As an example, your account rises from $25,000 to $50,000. It then subsequently drops to $40,000 but rises again to $60,000. The drawdown in this case would be $10,000 or -20%. Take note that drawdown does not necessarily have to correspond with a loss in your original account principal.

Return on Max Drawdown - We’ve added a dollar value for max drawdown along with a measure of return (return on max drawdown), which is calculated by dividing net profit by the max drawdown. In this way, max drawdown is considered the max capital investment. You can use the dollar value of max drawdown as a proxy for how much capital you need to trade the strategy. And, the higher the return on max drawdown, the better the strategy is in terms of risk/reward.

Percent Profitable - This is a metric that shows the number of winning trades divided by the number total trades.

Profit - The net profit made on the strategy for the backtest.

#trades per day - The average number of trades made per day using the strategy.

Profit / Day - The average profit made per day.

Profit / Trade - The average profit made per trade.

Lowest daily new profit - The worst performing day of the strategy in the backtest.

Highest daily net profit - The best performing day of the strategy in the backtest.

Profit Factor - Gross Profit divided by Gross Loss